Our Blog

The Watson Group

Click to see our 5 Star Reviews from our Amazing Fans Click to Call Now! Schedule a Tour Find out the Value of Your Home Our Guarantees

Click to see our 5 Star Reviews from our Amazing Fans Click to Call Now! Schedule a Tour Find out the Value of Your Home Our Guarantees

Recent:

Dont fear a housing market crash - heres why

With the increasing media coverage of changes in the housing market, it's no surprise that 67% of Americans are expecting a crash to occur within three years. Fortunately, recent evidence indicates this won't be anything like when homes plummeted in value 2008; today's market is far more stable and secure.

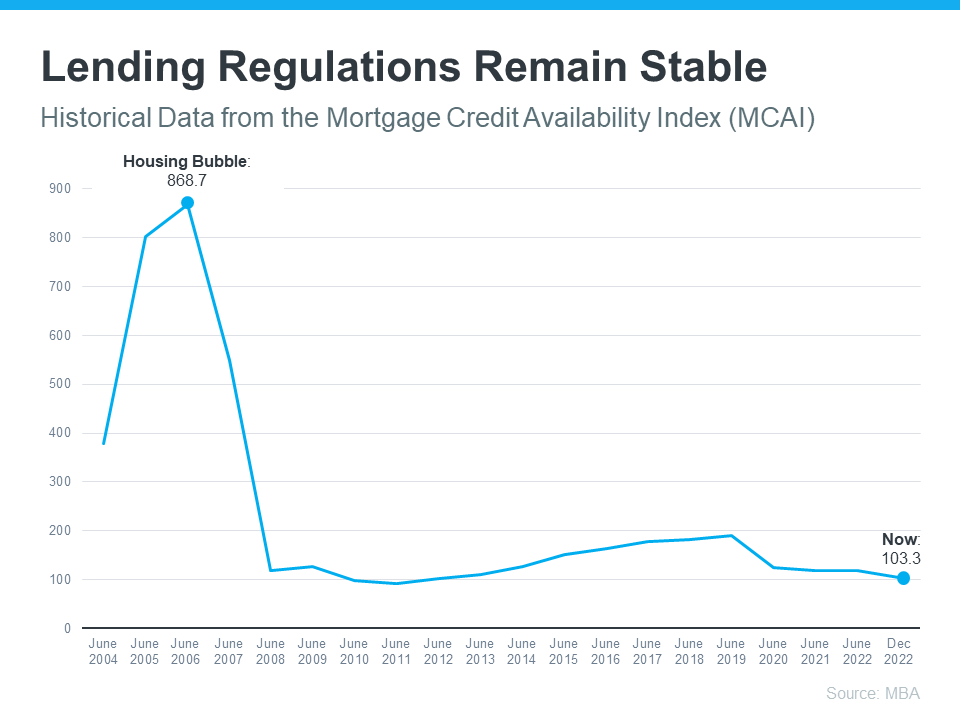

Back Then, Mortgage Standards Were Less Strict

In the years prior to the housing crisis, banks were deliberately driving up demand by weakening their lending criteria and allowing virtually anyone to qualify for a loan or mortgage. This made it far simpler than it is today for people to own homes.

Consequently, banks and other lending entities assumed a far greater risk when it came to both borrowers and the type of mortgages they provided. That caused an upsurge in defaults, foreclosures, and plummeting property values. Nowadays though, standards for mortgage seekers are much stricter than before due to improved oversight from lenders.

The graph below, utilizing data from the Mortgage Bankers Association (MBA), illustrates this story through its numbers: a higher number indicates that it is easier to get a mortgage; conversely, if the figure is low, securing one becomes more challenging.

This graph poignantly demonstrates how regulations have changed since the crash, allowing lenders to remain more responsible in their provision of credit. This has resulted in a significantly lower risk of foreclosures than what was seen during the previous crisis.

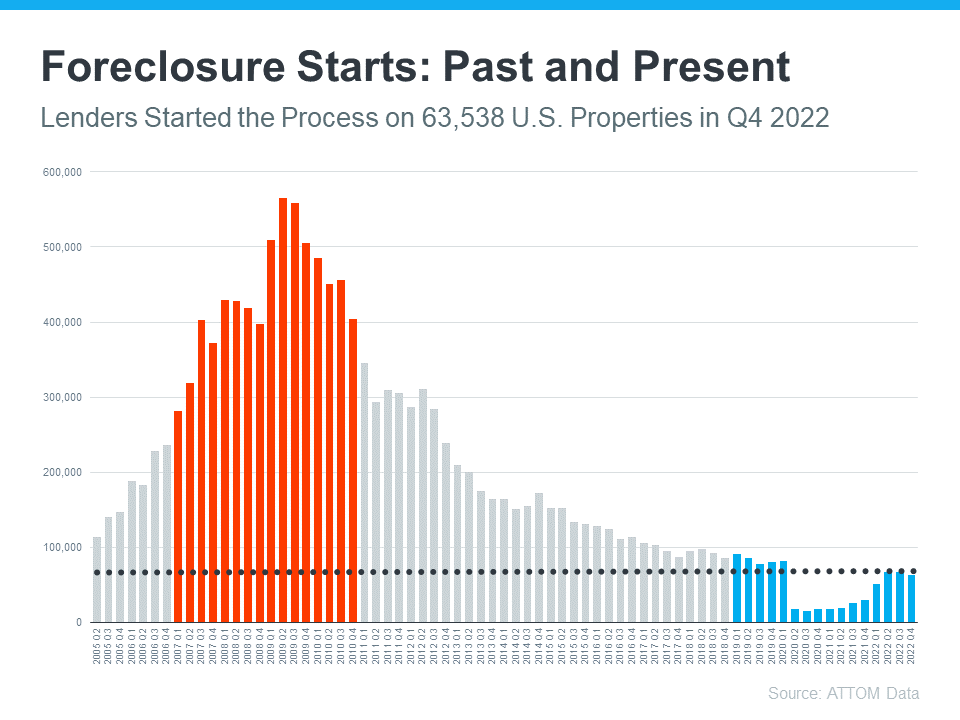

Foreclosure Volume Has Declined a Lot Since the Crash

The number of homeowners facing foreclosure took a sharp decline when the housing bubble burst, and since then has remained substantially lower. This is due to more qualified buyers today who are less likely to default on their loans. The chart below, composed with data from ATTOM, displays this significant contrast between now and last time:

Even with a slight surge in foreclosures, the overall number remains quite low. Furthermore, experts contend that foreclosures will not skyrocket as they did following 2008's market crash. Bill McBride of Calculated Risk elucidated how this played out before and why it is highly improbable to ever happen again, emphasizing the price of homes at the time.

“The bottom line is there will be an increase in foreclosures over the next year (from record level lows), butthere will not be a huge wave of distressed sales as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.”

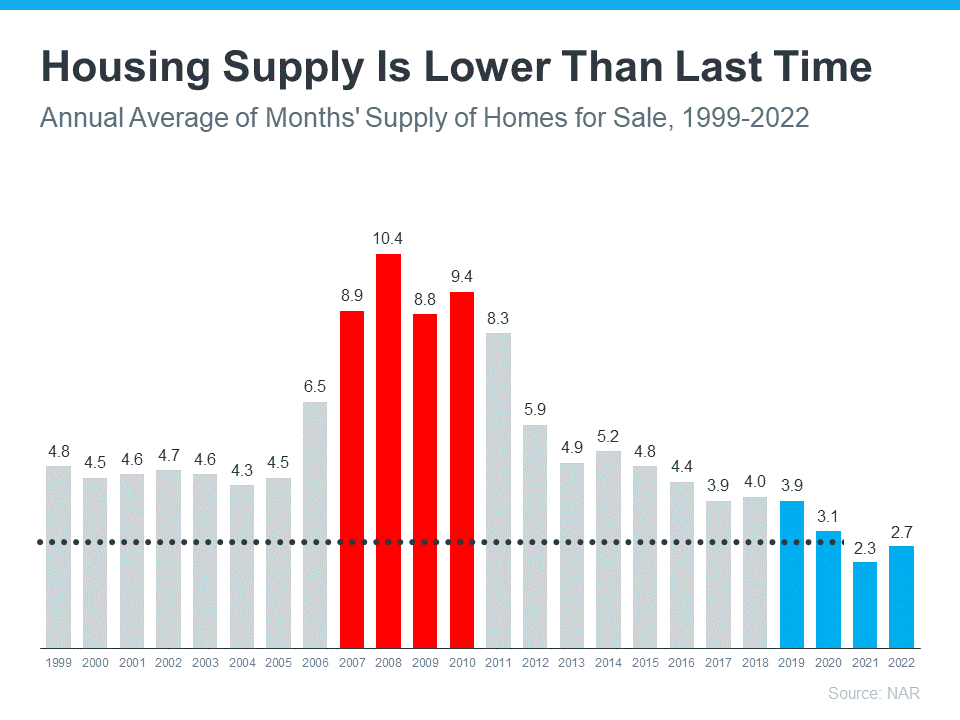

The Supply of Homes for Sale Today Is More Limited

Looking back, it was clear that the housing crisis caused an oversaturation of homes on the market. These were mainly foreclosures and short sales which resulted in a dramatic decrease in prices. Since early this year, there has been an increase in supply but overall inventory is still scarce given years of underbuilding properties.

The graph below, based on data provided by the National Association of Realtors (NAR), illustrates how unsold inventory today compares to that during a crash. At present, there is only 2.7-months’ supply available at the current sales rate--significantly lower than it was before--so despite some possibly overvalued markets potentially experiencing slight declines in prices, this time around we should be spared from an extensive and dramatic fall like last time.